You are currently viewing a placeholder content from Youtube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

For a 2°C compatible pathway, the G20 countries face an enormous investment gap. However, public spending will not suffice to finance the green transformation. In fact, a significant amount of private investment is required. It is therefore important to align the financial system – banking, capital markets and insurance – with sustainable development. To increase green investments and align financial markets with sustainable development, the G20 should 1) promote the standardization of green finance practices, 2) enhance the transparency of information by promoting disclosure standards for carbon and environmental risks; 3) support market development for green investments at a global level; and 4) support developing countries in developing and implementing national sustainable finance roadmaps.

Challenge

To successfully manage climate change and foster sustainable global growth the G20 need to implement a sustainability agenda both at the national and international level. By taking over the G20 presidency, Germany has the unique opportunity of following up on the progress made under China’s G20 presidency in developing a global green finance agenda.1 Green finance is defined as comprising “all forms of investment or lending that consider environmental effect and enhance environmental sustainability”.2

For a 2°C compatible pathway, the G20 countries face an enormous investment. The investment required in infrastructure for energy, transport, potable water supply and sanitation, as well as telecommunications over the next 15 years is estimated to be around US$ 80–90 trillion.3 Financial flows will need to be redirected from brown investments into sustainable investments. A scale-up of green investments will not only mitigate climate change, it will also foster economic growth and job creation. However, public spending will not suffice to finance the green transformation. The majority of investment must come from the private sector. It is therefore important to align the financial system – banking, capital markets and insurance – with sustainable development.

Moreover, it is important that the financial sector prepares itself for risk related to climate change and other environmental hazards. Three types of climate-related risk have been identified: (i) physical risk, i.e., the risk of economic and financial losses due to climate-related hazards; (ii) transition risk, i.e., the risk of financial losses related to regulatory and economic adjustments in a transition to a low-carbon economy; and (iii) liability risk, i.e., the risk that liability insurance providers have to cover claims related to losses arising from physical or transition risk from climate change.4

Aligning the financial system with sustainable development will require actions across the entire financial system and the involvement of all actors, including international financial institutions, banks, institutional investors, market-makers such as rating agencies and stock exchanges, as well as central banks and financial regulatory authorities.

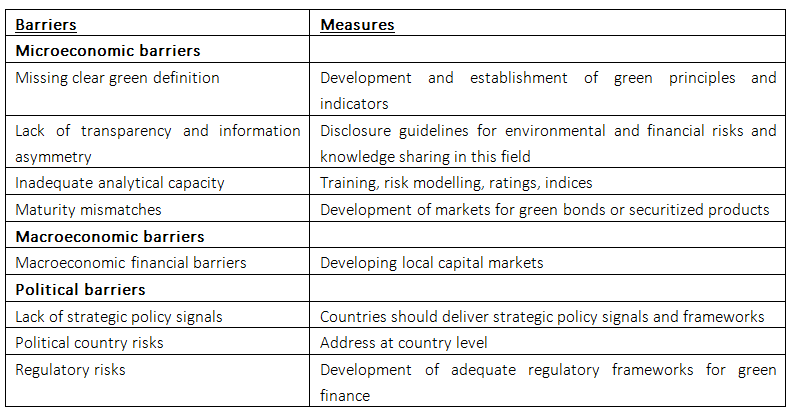

There are various microeconomic and macroeconomic as well as political barriers to mobilizing sufficient private capital for sustainable investment (Table 1). Microeconomic barriers include information asymmetry, maturity mismatches between long-term green investments and the relatively short-term time horizons of savers, and, inadequate analytical capacity.5

In addition to general macroeconomic barriers, such as exchange rate volatility, inflation, capital market controls and volatile GDP growth rates, there are specific macroeconomic financial barriers for green investments. Often, public fiscal capacity does not permit public spending on the green transition. In some developing and emerging markets, access to international capital markets is constrained, and local capital markets are under-developed and, therefore, not able finance green investments.6 Political risks include a lack of strategic policy signals, political country risks, regulatory risks and distorting policies.7

Proposal

Many G20 countries have already taken a number of steps to align their financial systems with sustainable development and address risks related to climate change (Box 1), ranging from market innovations to prudential action. Given the diversity of financial systems across the G20, it is clear that measures need to be tailored to the specific needs and circumstances of each country. While some of the challenges just discussed need to be tackled at the country level – including macroeconomic financial barriers or political country risks – the G20 could make important contributions by addressing clear green finance definitions, information asymmetry, inadequate analytical capacity and regulatory risks.

Box 1: Examples of green finance measures adopted by G20 countries

- Brazil: The BOVESPA Stock Exchange set up a Corporate Sustainability Index as early as 2005. The Banco Central do Brasil has introduced requirements for banks to monitor environmental risks, building on a voluntary Green Protocol from the banking sector. Brazil’s banking association (Federação Brasileira das Associações de Bancos, FEBRABAN) is developing a standardized assessment methodology and automated data collection system to monitor flows of finance for green economy sectors.

- China: The People’s Bank of China has introduced green bond standards and green banking regulation.

- France: The French government introduced mandatory climate-change-related reporting for institutional investors (Article 173 of France’s law on “energy transition for green growth”) starting in January 2016.

- Indonesia: The Indonesian financial regulatory authority (Otoritas Jasa Keuangan, OJK) published a Green Finance Roadmap in 2014.

- India: The Reserve Bank of India (RBI) has included lending to small renewable energy projects within the targets of its Priority Sector Lending requirement which require banks to allocate 40% of lending to key sectors such as agriculture and small and medium-sized enterprises.

- South Africa: Since 2010, environmental, social and governance (ESG) disclosure indicators have been introduced by the Johannesburg Stock Exchange.

- United Kingdom: In 2015, the Bank of England’s Prudential Regulation Authority published a report on the impact of climate change on the UK insurance sector.

- Germany: The German national Development Bank “Kreditanstalt für Wiederaufbau” (KfW) currently belongs to the largest Green Bond issuers worldwide.

In the following, we will focus on four policy areas that are universally relevant and that the G20 could promote either globally or nationally: 1) promote the standardization of green finance practices, 2) enhance the transparency of information by promoting disclosure standards for carbon and environmental risks; 3) support market development for green investments at a global level; and 4) support developing countries in developing and implementing national sustainable finance roadmaps.

(1) Promote the standardization of green finance practices

The G20 should promote a standardization of green finance practices in order to establish comparable markets for green financial assets across borders and impede greenwashing. The lack of commonly agreed definitions of what constitutes sustainable lending and investment practices contributes to a fragmentation of sustainable finance markets and delays the development of green financial markets.

While recognizing the diversity of financial systems, the G20 could promote developing and establishing green finance principles and indicators as well as reporting procedures.8The G20 could mandate the Financial Stability Board (FSB) to convene experts to develop green definitions and indicators for different products.

Building on existing market-driven and public initiatives, principles and guidelines for green finance should be developed for all asset classes, including bank credit, bonds and secured assets. For instance, the G20 should strive to harmonize standards in the green bond market and develop common green bond ratings criteria. The Green Bonds Principles established by the International Capital Market Association are a good example in this field.9

Once established, these standards also need to be monitored. The G20 should propose a monitoring system for assessing the implementation of green principles. In the same vein, the G20 should also support second-opinion providers and the guaranteed unrestricted disclosure of second opinions, as in the case of green bonds.

International regulatory standards such as Basel III for banks and Solvency II for insurers should consider environmental risks by including exceptions for capital and liquidity requirements for green investments.10 Whereas there is controversy over this recommendation, in particular within the private sector, because more regulation could impede market development, addressing environmental risks in solvency standards would contribute to ensuring financial market stability.11 In this vein, the G20 should mandate the FSB to develop an adequate regulatory framework for green finance.

The G20 countries should lead by example and should demand the adoption of green finance practices by public financial and non-financial institutions, including international organizations. This should also include supporting public-sector financial institutions to use shadow pricing in internal decision-making as an instrument for lowering climate-related risk in their investment portfolio.12

(2) Enhance the transparency of information by promoting disclosure standards for carbon and environmental risks

To address the problem of asymmetric information, it is crucial to enhance disclosure standards for carbon and environmental risks and related information flows. Climate change has financial impacts on the global economy and has endangered national and international capital markets. Investors often do not know to what extent specific sectors and companies have been affected by climate change. By the same token, investors are often not informed whether companies have been prepared and have addressed these risks.

The Financial Stability Board elaborated in its review mandated by G20 Finance Ministers and Central Bank Governors how the financial sector can take account of climate-related issues through voluntary disclosure. Initiatives focused on addressing transparency include the International Integrated Reporting Council, the Global Reporting Initiative and the Sustainability Accounting Standards Board. Disclosure reforms should not only include environmental and related financial risks but also set out the intended use of proceeds. The G20 should promote disclosure guidelines for environmental risks and related financial risks. 13 In this way environmental risks could be better integrated in financial market decision-making.

As recommended by the Task Force on Climate-related Financial Disclosures, climate-related financial disclosures should be included in the public financial filings of all financial and non-financial organizations with public debt or equity. Moreover, these organizations should also disclose their (i) governance structure and processes around climate-related risks and opportunities; (ii) strategy for dealing with actual and potential impacts of climate-related risks and opportunities; (iii) risk management, i.e., how the organization identifies, assesses, and manages climate-related risks; and (iv) the metrics and targets used to assess and manage relevant climate-related risks and opportunities.14 Making climate-related financial information publicly available will help investors to better understand the performance of their assets, consider the risks of their investments, and ultimately make more informed investment choices.

To improve transparency in the green finance markets and advance more informed investing, lending and insurance underwriting decisions, the G20 should promote knowledge sharing on environmental and financial risks among all stakeholders, be they private or public.15 The G20 should establish a regular dialogue, knowledge platforms, and round tables of investors, issuers, market makers, insurers, governments, NGOs and regulators. The Sustainable Banking Network is a good example in this field. By the same token, the G20 should support developing and standardizing prudential reporting requirements and promote the utilization of green indices.

(3) Support market development for green investments at a global level

While measures to standardize green finance practices and to enhance transparency can be expected to support market development, the G20 governments could take further joint actions to support the development of hitherto underdeveloped markets or create new markets that would facilitate green investments. A good example for the role that public institutions and policies can play in developing new markets is the market for green bonds, which has grown and matured significantly, not least due to issuances of green bonds by public banks and international financial institutions as well as regulatory frameworks developed in countries such as China and India.

Similarly, the G20 could facilitate the development of markets for sustainable infrastructure financing instruments that are customized to investor risk profiles across project lifecycles.16 In particular, the G20 could help establish regulatory and tax frameworks for infrastructure investment trusts and other investment vehicles to facilitate channelling investments into non-liquid, long-term green investments, while at the same time supplying liquid financial assets for investors. Examples include listed “Yieldcos” or investment trust funds that invest in green infrastructure. Likewise, G20 governments could support the development of green fintech through proportionate regulatory frameworks.17

(4) Support developing countries in developing national sustainable finance roadmaps

Taking account of its leadership role, the G20, together with the UN and other international organizations, should support developing countries in devising their own national green finance practices and frameworks. The G20 should develop a roadmap for the national implementation of the decarbonization goals laid down in the Paris Agreement and subsequently support developing countries to establish national roadmaps. Among others, the G20 should support developing countries in establishing legal, regulatory and institutional policy measures to align their financial systems with the stated sustainability goals. National sustainable finance roadmaps should be geared to country-specific circumstances and needs and be supported through technical assistance. Moreover, the G20 should support an exchange of experiences amongst G20 and developing countries, for instance through its GreenInvest platform.

Table 1: Barriers of green finance and policy measures

Source: Based on Berensmann / Lindenberg 2017, GFSG 2016, Glemarec et al., 2015.

References

- G20 (2016): G20 Leaders’ communiqué, Hangzhou summit, 4-5 September.

Available - Volz, U., Böhnke, J., Knierim, L., Richert, K., Röber, G.-M. & Eidt, V. (2015): Financing the Green Transformation: How to Make Green Finance Work in Indonesia. Basingstoke: Palgrave Macmillan.

- Bhattacharya, A., Meltzer, JP., Oppenheim, J., Qureshi, Z. & Stern, N. (2016): Delivering on sustainable infrastructure for better development and better climate. Brookings Institution. [Accessed 15 March]

Available - Batten, S., Sowerbutts, R. & Tanaka, M. (2016): Let’s talk about the weather: The impact of climate change on central banks. London: Bank of England.

- GFSG (Green Finance Study Group) (2016): G20 Green finance synthesis report. [Accessed 10 February 2017]. Alloisio I. & Carraro, C. (2015): Public-private partnerships for energy infrastructure: A focus on the MENA region, in: Caselli S., Corbetta, G. & Vecchi, V. (2015): Public–Private Partnerships for Infrastructure and Business Development. Principles, Practices, and Perspectives. Basingstoke: Palgrave Macmillan, pp. 149-1682015

GFSG 2016 - Glemarec Y., Bardoux, P.& Roy, T. (2015): The role of policy-driven institutions in developing national financial systems for long-term growth. UNEP Inquiry Working Paper no. 6, 2015. [Accessed 15 March 2017].

Available - Berensmann, K. & Lindenberg, N. (2017): Green finance across the universe, in: S. Boubaker, Cumming, D. & Nguyen D. (eds.), Ethics, ESG and Sustainable Prosperity. World Scientific Publishing, forthcoming.

- op cit, GFSG 2016

- ICMA (International Capital Markets Association) (2016): Green Bond Principles. Zurich.[Accessed 15 March 2017]

Available - Alexander, K. (2014): Stability and sustainability in banking reform. Are environmental risks missing in Basel III?. Cambridge and Geneva: University of Cambridge Institute for sustainability leadership in association with UNEP Finance Initiative. [Accessed 15 March 2017]; Campiglio, E. (2016): Beyond Carbon Pricing. The role of banking and monetary policy in financing the transition to a low-carbon economy. Ecological Economics 121, pp. 220–230.

Alexander (2014) - op cit, Berensmann & Lindenberg, 2017

- Bak, C., Bhattacharya, A., Edenhofer, O. & Knopf, B. (2017): Towards a comprehensive approach to climate policy, sustainable infrastructure, and finance. T20 Task Force on Climate Change and Finance.

Policy Brief on G20 Insights - op cit, GFSG 2016

- TCFD (Task Force on Climate-related Financial Disclosures) (2016): Recommendations of the Task Force on Climate-related Financial Disclosures, 14 December. [Accessed 15 March 2017]

Available - op cit, GFSG 2016

- OECD (Organisation for Economic Co-operation and Development) (2016): Progress report on approaches to mobilising institutional investment for green infrastructure.[Accessed 15 March 2017].

Available - UNEP Inquiry (2016): Fintech and sustainable development. Assessing the implications. [Accessed 15 March 2017].

Available